The spring semester started last week. I’m teaching Intermediate Accounting and Advanced Taxation this semester for Tarleton State University at their Waco satellite campus. Same as every spring semester, but this time, Hannah, my youngest, is in my Intermediate Accounting class. Kind of unusual, kind of nice…we’ll see how the semester goes. Her birthday is Tuesday, same day as our Intermediate Accounting class. I believe  we will be getting out early that night so we can go to dinner to celebrate her birthday! Here’s a picture of her birthday celebration in 2011, same boyfriend and we’ll be going to the same restaurant.

we will be getting out early that night so we can go to dinner to celebrate her birthday! Here’s a picture of her birthday celebration in 2011, same boyfriend and we’ll be going to the same restaurant.

I was preparing for class on Saturday morning, my routine, and did a little research on the history of accounting and thought I would share on my blog.

5th Century BC

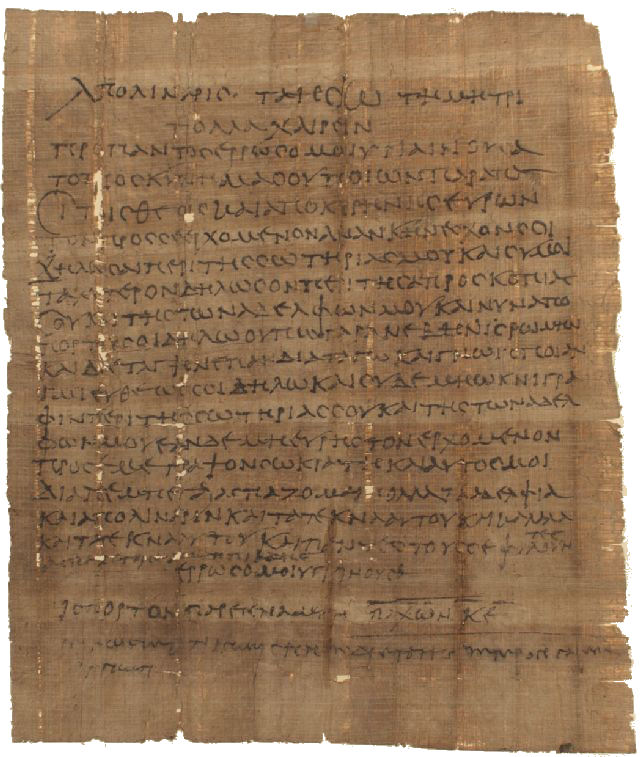

From as far back as the 5th century BC, there have been accounting records. Everyone wants to have information about their efforts and accomplishments. The Zenon papyri,  discovered in 1915, is believed to be one of the first formal accounting records. Zenon was a Greek who lived in Egypt and worked for Apollonios as a private secretary. Apollonios was an advisor to Ptolemy II who was in charge of the treasury and overseeing parcels of land. The discovery included 1,000 papers from Zenon which had information on constructions projects, agricultural activities and the like.

discovered in 1915, is believed to be one of the first formal accounting records. Zenon was a Greek who lived in Egypt and worked for Apollonios as a private secretary. Apollonios was an advisor to Ptolemy II who was in charge of the treasury and overseeing parcels of land. The discovery included 1,000 papers from Zenon which had information on constructions projects, agricultural activities and the like.

1000 A.D.

The Romans attempted to keep accounting records, but since they used letters for numbers, they could not develop a structured system of accounting. In the 1300s A.D. the Italians began to use the Arabic number system and arithmetic and, it is believed, they started the first double entry accounting system. Profit and loss statements and balance sheets first appeared in the 1600s. The accounting equation, Assets = Liabilities + Capital, first appeared in the early 19th century.

Industrial Revolution

The industrial revolution in the late 1800s brought the need for more formal accounting procedures. Back in those days any one could claim to be an “accountant”. In 1904 the formation of the International Congress of Accountants marked the initial development of an organized accounting profession in the U.S. The American Association of the University Instructors in Accounting was created in 1916. The membership attempted to create a standard accounting curriculum. For example, a student enrolled in a Cost Accounting course at Tarleton State University would be learning the same principles as a student enrolled in a Cost Accounting course at Baylor.

Stock Market Crash

Could the 1929 stock market crash been caused by poor accounting standards? I would venture to say poor accounting standards had something to do with it. Prior to the crash, companies created financial statements however they chose. There was no regulatory body and no real accounting standards. In the early 1930s Congress passed the Securities Act of 1933 and the Securities Exchange Act of 1934 which created the Securities & Exchange Commission. The SEC was given authority to set accounting standards, but  delegated that responsibility to the private sector (AICPA) and has primarily been a watch dog over publicly traded companies. In the years following, the AICPA through the Committee on Accounting Procedure, the Accounting Principles Board, and currently the Financial Accounting Standards Board, has created a set of accounting principles collectively referred to as GAAP, Generally Accepted Accounting Principles.

delegated that responsibility to the private sector (AICPA) and has primarily been a watch dog over publicly traded companies. In the years following, the AICPA through the Committee on Accounting Procedure, the Accounting Principles Board, and currently the Financial Accounting Standards Board, has created a set of accounting principles collectively referred to as GAAP, Generally Accepted Accounting Principles.

Sarbanes-Oxley

The Enron accounting scandal in 2001 created a stir among Congress, and as a result, they passed the Sarbanes-Oxley Act in 2002. Enron used special purpose entities to achieve off balance sheet financing. During the years Enron was engaging in this practice, the Financial Accounting Standards Board did not require the special purpose entities to be included in a consolidated financial statement if at least 3% of the special purpose entity was owned by an outside investor. Sarbanes Oxley created the Public Company Accounting Oversight Board which sets auditing standards. The Act also requires corporate presidents and CFOs to certify the accuracy of the financial statements. Publicly traded companies must attest to the effectiveness of their internal control system and the Act requires mandatory audit partner rotation every 5 years.

Effectiveness

Has Sarbanes-Oxley been effective in preventing misleading financial statements? Perhaps, but we still hear stories about companies who have “cooked the books” and doctored their financial statements to present a rosier picture to their shareholders. What is the answer? I suppose it goes back to ethics and maybe that’s why the Texas Board of Public Accountancy requires CPA s to have an ethics booster every two years and requires accounting students to have an entire 3 hour course in ethics before sitting for the CPA exam.